Learning how to stick to a budget is one of the most valuable financial skills you can build — but most people quit within weeks because traditional budgeting feels like punishment. If you want to stick to a budget without feeling deprived or restricted, these 7 simple steps will show you exactly how.

You know the cycle. You sit down with a spreadsheet, full of good intentions, and map out exactly where every dollar is going to go. It looks logical. It looks responsible. For about two weeks, you follow it religiously.

Then life happens. An unexpected expense. A bad week. A dinner out that wasn’t in the plan. And suddenly the budget feels broken — so you break it the rest of the way. You tell yourself you’ll start fresh next month. Next month comes and the cycle repeats.

The problem isn’t you. The problem is a model of budgeting built on restriction, guilt, and the expectation of perfection — and a model designed that way was always going to fail.

Real, sustainable budgeting looks completely different. It is built around awareness, flexibility, and intentional choice — not punishment. It gives you control over your money without making you feel controlled by your money. And it actually works over months and years, not weeks.

Here are 7 simple, practical steps to build a budget that you will actually stick to — and the tool that makes the whole process effortless.

Tired of Starting Budgets That Fall Apart Within Weeks?

The most common reason budgets fail is mental overload — too much manual tracking, too much friction, too much effort to maintain consistently.

Automatically calculates totals, categorises expenses, tracks income vs spending visually, and organises your entire financial picture in one place — so you spend your energy living your life, not updating spreadsheets. This is the system that actually makes these 7 steps stick.

Enter for a Chance to Go to the World Cup!

Step 1: Redefine What a Budget Actually Is

The first and most important step is a mental one — and most budgeting advice skips it entirely.

Most people associate the word “budget” with restriction, deprivation, and the slow removal of everything enjoyable from life. That association is why so many people resist budgeting or abandon it at the first sign of struggle. They are not avoiding the spreadsheet. They are avoiding the feeling the spreadsheet represents.

Here is the reframe that changes everything: a budget is not a list of things you can’t have. It is a plan for where your money goes.

The difference is profound. “I can’t spend money on that” is a passive position — you are being controlled. “I’m choosing where my money goes” is an active one — you are in control. Same financial reality, completely different psychological relationship with it.

A budget is a roadmap. It doesn’t tell you you can’t travel — it helps you make sure you’re travelling somewhere you actually want to go. It ensures your money is directed toward what genuinely matters to you — your bills, your savings, your goals, your life — rather than disappearing without trace into purchases you barely remember making. This mindset shift is the foundation that makes it possible to stick to a budget long term.”

When you approach budgeting as an empowerment tool rather than a punishment system, the entire experience changes. And that change in framing is the foundation everything else is built on.

Step 2: Start With Awareness — Not Restrictions

The most common budgeting mistake is starting by cutting expenses before you understand your actual spending patterns. This produces a budget built on assumptions rather than data — and assumptions are almost always wrong.

Before you change a single spending behaviour, spend 30 days simply observing where your money goes. No judgment. No adjustments. Just honest tracking — every purchase, every subscription, every coffee, every impulse buy.

What you discover will almost always surprise you.

Subscriptions you’ve been paying for services you forgot you had. Small daily purchases that feel insignificant individually but collectively account for hundreds of dollars monthly. Spending categories you assumed were high that are actually manageable. Categories you thought were fine that are quietly draining your account. Awareness of your spending patterns is what makes it realistic to stick to a budget without guessing.”

Awareness produces clarity. Clarity produces better decisions. When you build your budget on actual data about your actual spending patterns rather than optimistic guesses, every subsequent step becomes more realistic, more achievable, and more sustainable.

The fastest path to a budget that sticks is starting not with restrictions but with honesty about where you currently are.

Step 3: Build a Guilt-Free “Freedom” Category

This is the step most traditional budgeting advice completely ignores — and its absence is why most budgets eventually collapse.

The human brain does not respond well to absolute deprivation. When you eliminate everything enjoyable from your financial plan — coffee, dining out, hobbies, small indulgences that bring daily pleasure — you create a budget that is emotionally unsustainable. You can white-knuckle it for a few weeks. But the resentment builds, the deprivation feels intolerable, and eventually you either abandon the budget or spend recklessly to compensate.

The solution is to plan for joy deliberately. Create a dedicated “Freedom Category” — a guilt-free spending allowance for things you genuinely enjoy. This might be:

- $50–$100 per month for dining out

- A weekly small treat within a set amount

- Entertainment, hobbies, or personal purchases

- Whatever brings you genuine pleasure in the range you can afford

The psychological key is that when this spending is planned and accounted for, it stops carrying guilt. You are not “breaking” the budget by buying a coffee — you are using your planned Freedom allocation. The guilt dissolves because the choice was already made consciously. And when guilt dissolves, the rebellious spending that guilt produces dissolves with it. Planning for joy is what allows you to stick to a budget without feeling restricted or deprived.”

Budgeting does not mean no. It means choice — and planning for the choices that make life enjoyable is as important as planning for the choices that build financial security.

Step 4: Choose a Budgeting Method That Matches Your Personality

There is no single correct way to budget — and one of the most common budgeting mistakes is adopting a method that doesn’t suit your personality, lifestyle, or cognitive style, and then concluding that budgeting doesn’t work when it fails.

The best budgeting method is the one you will actually use consistently. Here are the most effective approaches:

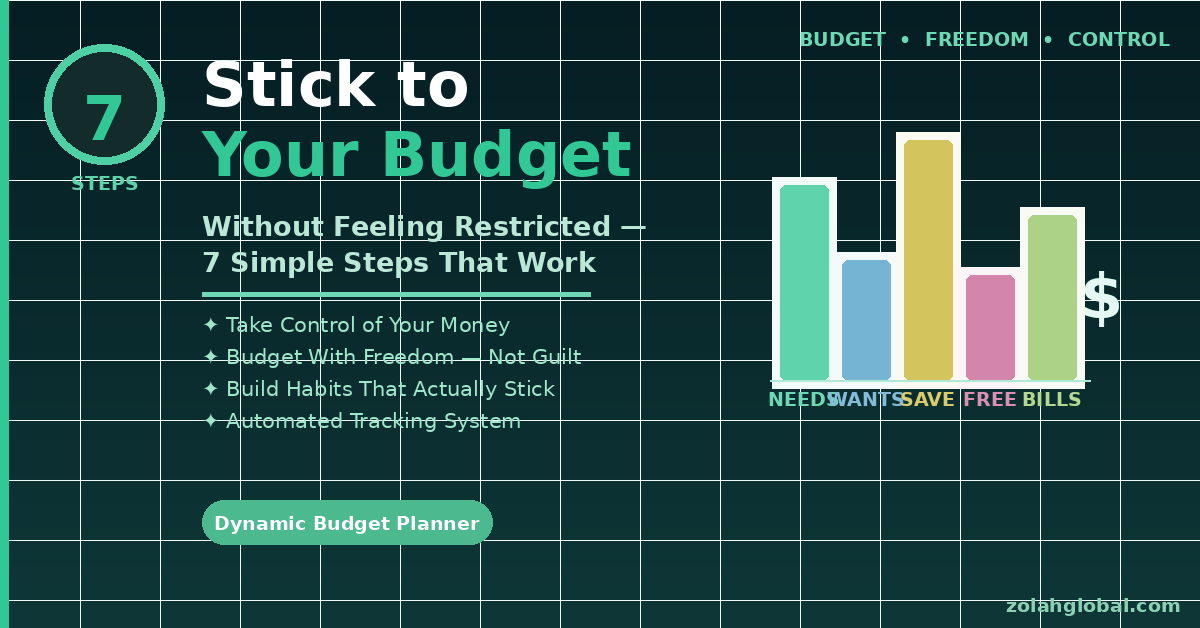

The 50/30/20 Rule — allocate 50% of after-tax income to needs (housing, utilities, food, transport), 30% to wants (dining, entertainment, lifestyle), and 20% to savings and debt repayment. Simple, memorable, and effective for people who prefer broad categories over granular detail.

Category-Based Budgeting — assign specific amounts to each spending category: rent, utilities, groceries, transport, entertainment, personal care, and so on. More detailed and specific, better suited to people who want precise control over each area.

Weekly Spending Caps — break your monthly disposable income into weekly allowances. Psychologically easier for many people to track — a weekly $200 budget feels more concrete and manageable than a monthly $800 one.

Automated Tracking — use tools, spreadsheets, or apps that categorise and calculate automatically, removing the manual tracking burden that causes most budgets to be abandoned.

Match the method to the person, not the other way around. A complicated system that tracks every penny might sound thorough, but if it creates friction that leads to avoidance, it is worse than a simple system that gets used every day.

Step 5: Build Flexibility Into the Foundation

A rigid budget is a fragile budget. Life is unpredictable — and a financial plan that cannot accommodate life’s unpredictability will be abandoned the first time reality diverges from the plan.

Unexpected car repairs. Medical expenses. A social event that costs more than anticipated. Income that varies month to month. These are not budget failures — they are life. And a sustainable budget treats them as such. Flexibility is what separates people who stick to a budget for years from those who quit after weeks.

Build flexibility into your system deliberately:

Create a buffer category — a small monthly allocation specifically for unexpected expenses. Even $50–$100 per month prevents unplanned spending from feeling like a crisis.

Practice the “move, don’t fail” principle — when you overspend in one category, move money from another rather than declaring the budget broken. You are adjusting a plan, not abandoning it.

Review monthly, not daily — daily scrutiny creates anxiety. Monthly review creates learning. Ask: What category needs adjustment? What worked well? What should I do differently next month?

The goal is not a perfect month. The goal is a sustainable system that keeps you engaged with your finances across months and years — adapting as your life adapts, rather than collapsing under the first unexpected pressure.

Step 6: Prioritise Consistency Over Perfection

This is the most important mindset principle in all of personal finance — and the one most people never internalise.

Perfection kills progress. An overspent week, a miscalculated category, a month where circumstances derailed your best intentions — none of these are failures. They are normal. They are what happens when real people with real lives try to manage money in an unpredictable world.

What determines long-term financial success is not the absence of imperfect months. It is the commitment to returning to the system after imperfection — reviewing, adjusting, learning, and continuing. Consistency — not perfection — is the real secret to stick to a budget that transforms your finances.”

Every person who has achieved meaningful financial progress has had months that didn’t go to plan. The difference between them and the people who never make progress is not that they budgeted perfectly. It is that they didn’t let imperfect months become a reason to stop.

Monthly review is the habit that makes this possible. Fifteen minutes at the end of each month to look at what happened, understand why, and make one or two adjustments going forward. That fifteen minutes, repeated consistently over a year, produces more financial progress than any perfect month ever could.

Step 7: Remove the Mental Overload With the Right Tools

The final — and often most practically impactful — step is removing the friction that causes most people to quietly abandon budgeting despite the best of intentions.

Manual tracking is exhausting. Updating spreadsheets, categorising every transaction, calculating totals, remembering to record every purchase — it requires sustained cognitive effort that competes with everything else demanding your attention. Over time, the mental cost of maintaining the system exceeds the perceived benefit of having it, and tracking quietly stops. The right tools remove the friction that stops most people from being able to stick to a budget consistently.

The solution is automation. A system that calculates totals automatically, categorises expenses without manual input, and visualises your income versus spending at a glance removes the friction that kills consistency.

This is exactly what the Ultimate Dynamic Personal Budget Planner provides — a complete, automated budgeting system built in Google Sheets that works with you rather than requiring constant effort from you.

Automate the Hard Part — So You Can Focus on the Part That Actually Changes Your Finances

Everything you need to implement all 7 steps in this guide without the manual tracking burden that causes most budgets to fail. Totals calculated automatically. Spending categorised clearly. Income versus expenses tracked visually. One system. One place. Finally under control. Thousands are already using it. Your financial clarity starts today.

Putting It All Together: Your Budget, Your Life

These 7 steps work together as a system, not as isolated tips. The mindset shift in Step 1 makes everything else possible. The awareness from Step 2 makes the categories in Step 3 realistic. The right method from Step 4 makes the flexibility in Step 5 practical. The consistency focus of Step 6 sustains everything long-term. And the right tools from Step 7 remove the friction that would otherwise erode the whole structure over time.

This is not about restricting yourself into financial responsibility. It is about building a relationship with your money that is honest, intentional, and sustainable — one that supports the life you want to live rather than working against it.

Final Thoughts: Financial Control Is Freedom — Not Restriction

The people who manage money well are not people who never enjoy themselves. They are people who know where their money goes, make intentional choices about it, and have built systems that make those choices easy to sustain.

A good budget gives you clarity. A great budget gives you confidence. The best budget gives you the freedom to enjoy your money without anxiety — because you know your bills are covered, your savings are growing, and your fun spending is planned and guilt-free.

Start with one step today. The awareness exercise from Step 2 requires nothing but honesty and 30 days of observation. The freedom category from Step 3 requires a single decision about what brings you joy and how much you’ll allocate to it.

Build from there. Be consistent, not perfect. Use the right tools. And watch your relationship with money transform from a source of stress into a source of confidence.

Take Control of Your Money — Starting With the System That Does the Hard Work for You

You have the strategy. All that’s left is having a system that makes following it effortless — so your budget stops being something you have to fight to maintain and starts being something that just works.

Join thousands of people who stopped fighting their budget — and started using a system that makes financial clarity automatic. Your money deserves a plan. You deserve the confidence that comes with having one.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Individual financial situations vary. Consult a qualified financial professional for personalised guidance.

Disclosure: This post contains affiliate links. If you purchase through our link, we may earn a small commission at no extra cost to you. We only recommend products we believe deliver genuine value.